Page 145 - CCRT-Annual-Report-2017-18

P. 145

Separate Audit Report of the Comptroller & Auditor General of India

on the accounts of Centre for Cultural Resources and Training

for the year ended 31 March 2018

We have audited the attached Balance Sheet of Centre for Cultural Resources and Training (CCRT), New Delhi as at

31 March, 2018. Income & Expenditure Account and Receipts & Payments Account for the year ended on that date

under Section 20(1) of the Comptroller and Auditor General’s (Duties, Powers & Conditions of Service) Act, 1971. The

audit has been entrusted for the period up to 2018-19. These financial statements are the responsibility of the CCRT’s

management. Our responsibility is to express an opinion on these financial statements based on our audit.

2. This Separate Audit Report contains the comments of the Comptroller and Auditor General of India

(C&AG) on the accounting treatment only with regard to classification, conformity with the best accounting practices,

accounting standards and disclosure norms etc. Audit observation on financial transactions with regard to compliance

with the Law, Rules & Regulations (Propriety and Regularity) and effeciency-cum performance aspects, etc., if any,

are reported through Inspection Reports/C&AG's Audit Reports separately.

3. We have conducted our audit in accordance with auditing standards generally accepted in India. These

standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial

statements are free from material misstatements. An audit includes examining, on a test basis, evidences supporting the

amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used

and significant estimates made by management as well as evaluating the overall presentation of financial statements.

We believe that our audit provides a reasonable basis for our opinion.

4. Based on our audit, we report that :

i. We have obtained all the information and explanations, which to the best of our knowledge and belief were

necessary for the purpose of our audit.

ii. The Balance Sheet and Income & Expenditure Account/Receipts & Payments Account dealt with by

this report have been drawn up in the Uniform Format of Accounts prescribed by Ministry of Finance,

Government of India.

iii. In our opinion, proper books of accounts have been maintained by the CCRT in so far as it appears from

our examination of such books.

iv. We further report that :

A. Balance Sheet

A.1 Assets

A.1.1 Fixed Assets (Schedule 8)- ` 60.80 crore

A.1.1.1 There were missing library books of ` 0.59 lakh and obsolete items of ` 57.34 lakh, which were not

deducted from fixed assets shown in balance sheet of annual accounts for the year 2017-18. This has

resulted in overstatement of Fixed Assets as well as Capital Fund by ` 57.93 lakh.

This was also reported in the previous year’s report but remedial action was not taken by the Management despite

assurance given by it.

A.1.2 Current Assets, Loans, Advances etc. (Schedule 11)- ` 2.27 crore.

A.1.2.1 CCRT had depicted the following advances of ` 3.38 lakh in the annual accounts for the year 2017-18, which

remained outstanding for long periods:

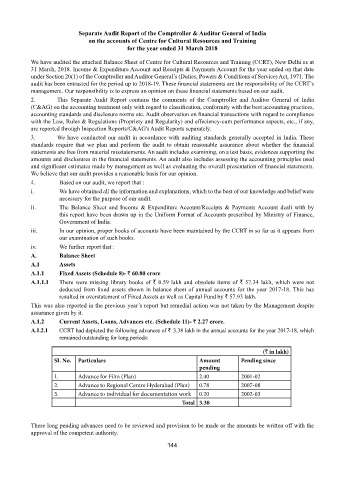

(` in lakh)

SI. No. Particulars Amount Pending since

pending

1. Advance for Film (Plan) 2.40 2001-02

2. Advance to Regional Centre Hyderabad (Plan) 0.78 2007-08

3. Advance to individual for documentation work 0.20 2002-03

Total 3.38

These long pending advances need to be reviewed and provision to be made or the amounts be written off with the

approval of the competent authority.

144